[ad_1]

Key Takeways

Spot volume remains low and liquidity thin in Bitcoin markets

Only 2.7% of the supply has moved in the last week; 7% has moved in the last month

This compares to 7% of the total supply of Bitcoins which are likely lost

Uncertainty is high due to tightening regulation and the macro climate

With institutions filing ETFs and launching exchanges, the liquidity picture may change drastically in the future

Market participants will know that if anything is true about the Bitcoin market over the last year, it’s that it has been incredibly illiquid.

Market depth was thin anyway by the time November 2022 rolled around. Then came the FTX implosion and an Alameda-sized hole in order books. Bankman-Fried’s trading firm was also one of the largest market makers around, and market depth has never recovered since its demise.

The effect has worsened in the last few months as a result of the regulatory clampdown in the US. We saw a host of market makers wind back operations in the US, including Jump Crypto and Jane Street in May (ironically, Bankman-Fried worked for the latter before founding Alameda).

We put together a data dive on this back in March, but in looking at the balance of stablecoins on exchanges below, we can see 60% have left exchanges in just over six months, amounting to $26 billion.

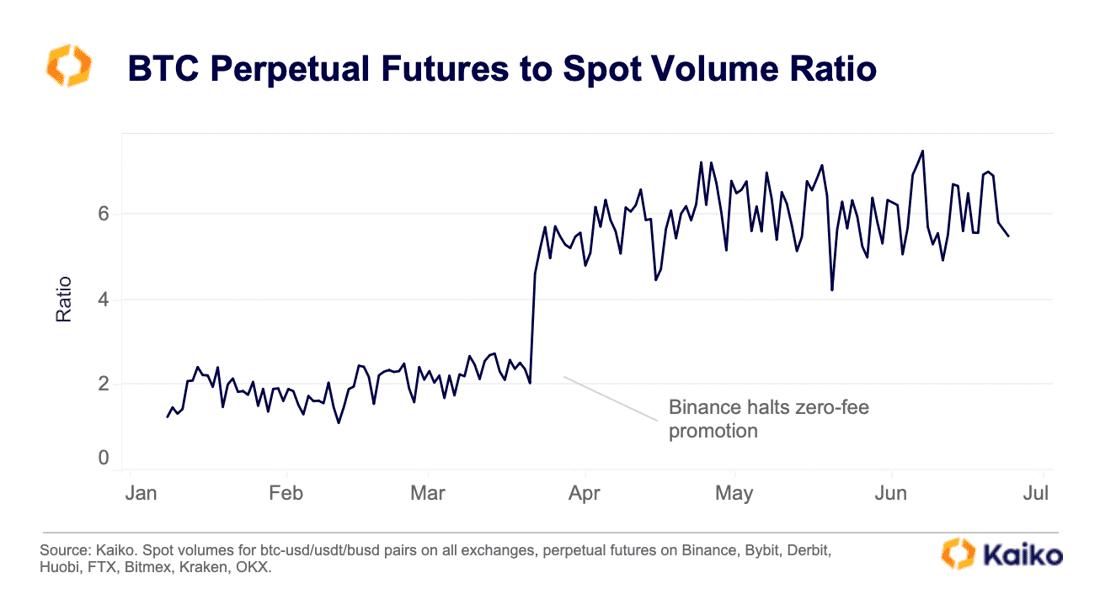

We can also see below that much of the volume earlier in the year was derived from Binance via zero-fee promotions. Once this promotion ceased, the futures-to-spot volume ratio jumped, highlighting that even that thin level of spot volume was propped up somewhat artificially by zero fees (chart via Kaiko).

Indeed, one of the (many) charges facing Binance is that the exchange engaged in “targeted wash trading” to increase volumes. Therefore, the shallow volume could be even shallower in reality.

By now, we all know this. I want to take a moment to assess the supply side of the equation, however. From day 1, Bitcoin has possessed two qualities which make it ever-so-intriguing: a final capped supply of 21 million coins and a pre-determined schedule at which those coins are released (with the supply cap slated to be hit in the year 2140).

As of today, 92.4% of the Bitcoin supply has already been released. By pulling some on-chain data, I have plotted below the percentage of coins which have moved in the last month against the total supply. This gives some indication into how many coins are moving due to trading activity.

The chart shows 1.4 million coins have moved in the last month, equivalent to 7% of the circulating supply. In truth, one month is likely too broad a time horizon. Narrowing it to a (still conservative) one week in the next chart shows around half a million coins moving, around 2.7% on the total supply.

These charts highlight further how few Bitcoins are actually moving around these days. In fact, if I can use one more chart to illustrate the scarcity at play here, let’s look at this next one which layers in an estimate of lost coins. These lost coins are estimated by Glassnode and are coins which have been inactive since before the launch of the first Bitcoin exchange in July 2010 (as coins from pre-July 2010 are spent, this estimate converges to the real number of lost coins; it’s not a perfect measure, but a good estimate).

The chart shows that 7.5% of the total supply can be currently estimated as lost (Satoshi Nakamoto’s stash is included here). That means that it is roughly the same number as the amount of coins that have moved in the last month, and triple the number of coins that have moved in the last week.

Therefore, only a small portion of the supply is moving for Bitcoin. On one hand, this sounds bullish – one oft-repeated mantra within the space is that a dwindling supply will inevitably lead to an uptick in price. But this is only the case if the thin supply is matched by an uptick in demand.

When we look at order books and market depth over the last nine months, the shallow liquidity is a concern. However, there have been several important developments in the last two weeks that provide hope that this may change. Blackrock, the world’s largest asset manager, filed for a spot Bitcoin ETF, only to be swiftly followed by fellow giant Fidelity. There is also the launch of the exchange EDX, backed by trad-fi giants Fidelity, Schwab and Citadel.

Even the tightening regulatory noose around Binance could help provide a clearer picture for the future of the space and give investors confidence that something is finally being done to clean up the opaque nature of so much of the industry.

In conclusion, it feels quite likely that we will be looking back upon these uber-thin liquidity conditions in awe in a couple of years’ time. Uncertainty is extreme right now, both with regard to regulation but also the macro picture. There will come a day when that won’t be the case, and things may be very different as a result. But as of right now, it’s thin out there.

[ad_2]

Source link