Washington Draws a New Line for Crypto Markets

The SEC and CFTC have finally done something the U.S. crypto market has waited years to see: they issued a joint interpretation laying out how federal securities law applies to crypto assets and related transactions. The move does not create a new statute, and it does not end regulatory uncertainty overnight, but it does draw a much clearer jurisdictional line between crypto assets that are treated as securities and those that are not. Just as importantly, it signals a coordinated approach between the two agencies at a moment when Congress is still working toward a broader market structure law.

The market impact is not simply legal. This is one of the first major U.S. regulatory documents to openly state that most crypto assets are not themselves securities, while also explaining how a token that is not a security can still be sold as part of an investment contract depending on how it is marketed and distributed. That distinction is likely to shape how exchanges, issuers, token projects, and investors frame crypto assets going forward.

What the SEC and CFTC actually released

On March 17, 2026, the SEC published an interpretive release titled Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets. The CFTC formally joined the interpretation and said it will administer the Commodity Exchange Act consistently with the SEC’s interpretation. The SEC page identifies the action as an interpretive final release, not a new act of Congress, and the CFTC’s own press release presents it as coordinated agency guidance.

That distinction matters. This is not a permanent legislative settlement of crypto regulation in the United States. It is an agency interpretation intended to clarify how existing securities law applies right now, while Congress continues to work on a broader statutory framework. Even the SEC’s own release frames the interpretation as complementing Congressional efforts rather than replacing them.

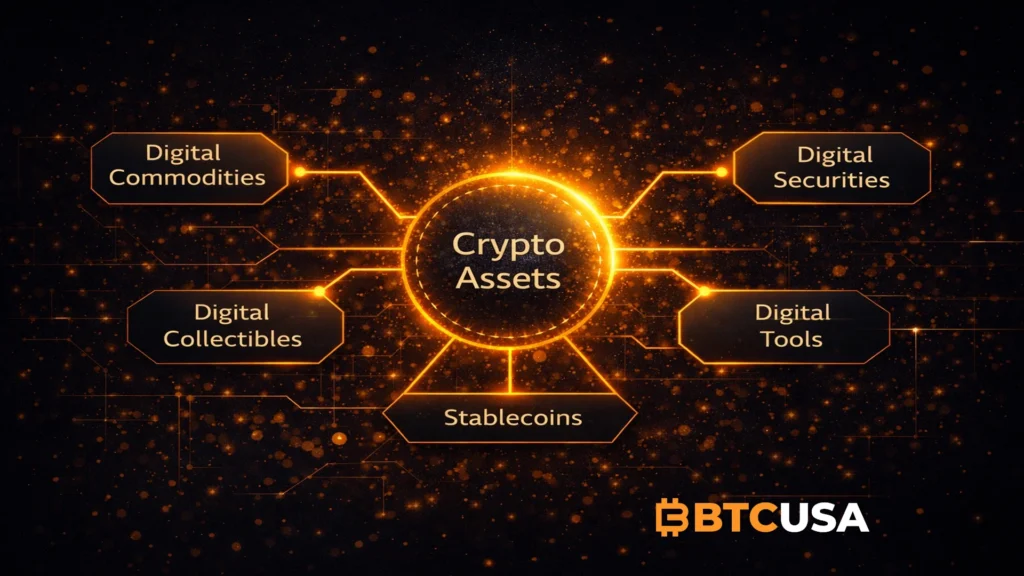

The new token taxonomy is the headline shift

The SEC’s fact sheet says the interpretation creates a more coherent token taxonomy built around five buckets: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. That may sound bureaucratic, but it is probably the most market-relevant part of the document because it gives participants a clearer vocabulary for thinking about regulatory treatment across different token types.

According to the fact sheet, digital commodities are not securities. These are crypto assets that are intrinsically linked to the programmatic operation of a functional crypto system and derive their value from that operation plus supply-and-demand dynamics, rather than from the expectation of profits based on the essential managerial efforts of others. Digital collectibles are also not securities, nor are digital tools with practical use cases such as credentials, memberships, tickets, or title instruments. The SEC also says GENIUS Act payment stablecoins issued by permitted issuers are not securities, while tokenized traditional financial instruments remain securities.

In practical terms, this is the clearest formal statement yet from the SEC that the agency sees a large category of functional crypto assets as outside the definition of a security. That does not mean every token escapes scrutiny, but it materially changes the tone from the earlier enforcement-first era described in the SEC’s own fact sheet.

BTC, ETH, SOL, XRP, ADA, LINK and others are explicitly listed as digital commodities

One of the most important passages in the full interpretive release appears in the section defining digital commodities. There, the SEC gives named examples of crypto assets it concludes are digital commodities based on their characteristics, terms, and functions as of the date of the release. The list includes Aptos, Avalanche, Bitcoin, Bitcoin Cash, Cardano, Chainlink, Dogecoin, Ether, Hedera, Litecoin, Polkadot, Shiba Inu, Solana, Stellar, Tezos, and XRP. The same passage also notes that Algorand and LBRY Credits are digital commodities as examples even though they do not underlie CFTC-supervised futures contracts.

That is a major signal to the market. It is not just a generic principle; it is an explicit regulatory example set. The SEC also explains that these named examples were selected in part because, as of the release date, each underlies a futures contract available for trading on a designated contract market under CFTC oversight, while also clarifying that this is not a prerequisite for digital commodity status.

For investors, that means the document goes much further than vague “case by case” rhetoric. It effectively creates a practical reference list of high-profile tokens the agency currently views as non-security crypto assets.

Why the investment contract distinction still matters

This does not mean every sale, promotion, or distribution involving those assets is automatically outside securities law. In fact, the SEC repeatedly stresses the opposite. The interpretation explains how a non-security crypto asset may become subject to an investment contract when an issuer induces an investment of money in a common enterprise through representations or promises of essential managerial efforts from which buyers reasonably expect profits. It also explains how that status can end once those promises are fulfilled or fail.

This may become the single most misunderstood part of the release. The token itself can be a non-security crypto asset, while the offering or surrounding arrangement can still trigger securities-law treatment as an investment contract. The SEC even states in the full release that the fact a non-security crypto asset is subject to an investment contract does not transform the asset itself into a security.

That is a subtle but powerful shift. It opens the door to a world where regulators focus less on labeling the token forever and more on the circumstances of issuance, promotion, and managerial promises. For the crypto industry, that is likely a more workable framework than the older all-or-nothing logic, but it still leaves room for enforcement when projects market tokens as profit vehicles tied to team execution.

Staking, mining, wrapping, and certain airdrops get clearer treatment

Another major win for the industry is the SEC’s treatment of protocol mining, protocol staking, wrapping of non-security crypto assets, and certain airdrops. The fact sheet says protocol mining, protocol staking, and wrapping of a non-security crypto asset do not involve the offer and sale of a security as described in the interpretation. It also says certain airdrops do not involve an investment of money under Howey.

That does not mean every activity loosely described as “staking” or “airdrops” is safe in every context. The protection comes from the covered activity as described in the interpretation, not from the label alone. Still, this is one of the strongest official signals yet that core protocol participation activities are not automatically securities transactions. For exchanges, validators, staking providers, and protocols, that clarification could be one of the most commercially important parts of the release.

Stablecoins are not fully off the hook

The stablecoin language is more nuanced than some headlines will suggest. The SEC fact sheet says GENIUS Act stablecoins, defined as payment stablecoins issued by permitted payment stablecoin issuers, are not securities. But the text does not say every stablecoin in the market is now categorically outside securities law. The treatment turns on the specific GENIUS Act definition and issuer status.

That means the market should be careful not to flatten this into a blanket “stablecoins are not securities” message. The interpretation clearly gives a regulatory lane to qualifying payment stablecoins, but it leaves room for different treatment where a token has additional investment-like features or does not fit the statutory definition referenced by the SEC.

Why this is a jurisdictional win for the CFTC

The CFTC’s role here is not decorative. The SEC release says market participants should review the interpretation to better understand regulatory jurisdiction between the SEC and CFTC, and the CFTC’s own press release says it joined the interpretation to guide administration of the Commodity Exchange Act consistently with the SEC’s view. That effectively reinforces the idea that non-security crypto assets can fall within the CFTC’s commodity jurisdiction.

The real significance is structural. If a wider class of major crypto assets is treated as digital commodities rather than securities, that strengthens the CFTC’s position in overseeing large parts of the spot-linked ecosystem, especially where derivatives and futures markets already exist. It does not hand the CFTC full spot-market authority by itself, but it materially strengthens the market-structure narrative the industry has been pushing for years. This last point is an inference from the agencies’ own framing and the document’s jurisdictional design, rather than an explicit line stating “the CFTC now fully governs crypto spot markets.”

What this means for crypto markets now

For the market, this is not just legal housekeeping. It lowers one of the biggest long-running uncertainty premiums in U.S. crypto: whether large-cap tokens might continue to be treated as suspect securities by default. The fact that the SEC itself now lists BTC, ETH, SOL, XRP, ADA, LINK, DOGE, AVAX, APT, DOT, HBAR, LTC, BCH, XLM, XTZ, and SHIB as digital commodities changes the regulatory backdrop for exchanges, market makers, institutional desks, and long-term asset allocators.

At the same time, the release does not create a free pass for token issuers. If a team sells a token by emphasizing managerial execution, future platform development, or profit expectations tied to its own efforts, that arrangement can still look like an investment contract. So the biggest winners may be mature, already-functional protocols and secondary-market infrastructure, while speculative token launches and narrative-driven primary distributions may still face meaningful legal pressure.

BTCUSA Takeaway

This is one of the most consequential U.S. crypto regulatory documents in years because it does something the market has been demanding since the first wave of token litigation: it separates the nature of the asset from the nature of the offering. In doing so, the SEC and CFTC have moved the conversation away from blanket token labeling and toward a more functional framework centered on digital commodities, covered protocol activity, and context-specific investment contracts.

The bullish read is straightforward: a large share of the crypto market just got a much clearer path away from automatic securities treatment. The sober read is equally important: this is still interpretation, not permanent statute, and projects can still cross back into securities-law territory depending on how they raise money and market tokens. Congress can lock the framework in place. Until then, this document is a bridge, but it is a very important bridge.